Acomba GO

Acomba GO

Acomba

Acomba

Acomba Construction

Acomba Construction Perform a bank reconciliation

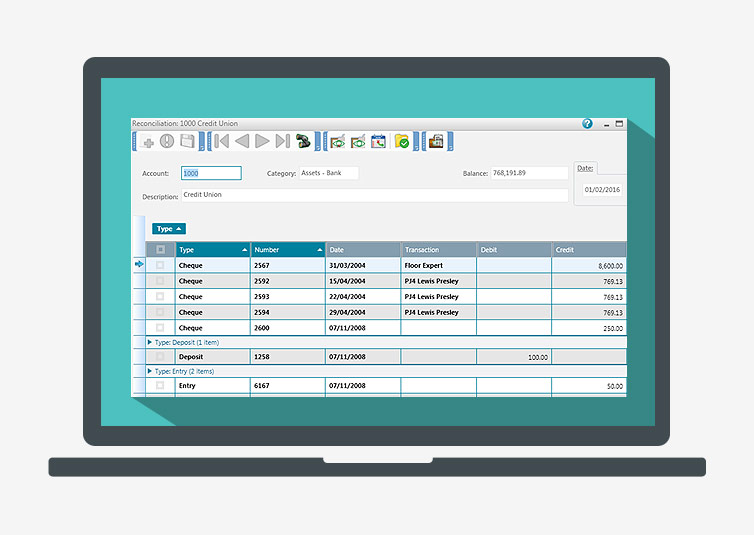

Reconciliation consists in comparing two accounts on a specified date, in order to check the consistency of balances and find differences. The most common reconciliation is to compare an account from the Assets – Bank category to the statement from the bank.

To create a reconciliation, proceed as follows:

- In the General Ledger tab, Transactions group, click the Reconciliations arrow button and select Create a Reconciliation. The Reconciliation window is displayed.

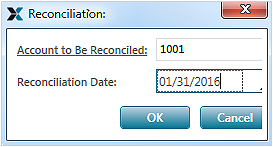

- In the Account to Be Reconciled field, select the account number or double-click the field to select one from the list.

- Enter the Reconciliation Date or click the lower right corner of the field to display the calendar.

- Click OK. The Reconciliation window is displayed.

- In the first column, select the transactions to reconcile by checking the appropriate boxes. The other columns display the information on the transactions and are in read-only.

- To accelerate the selection of transactions, click

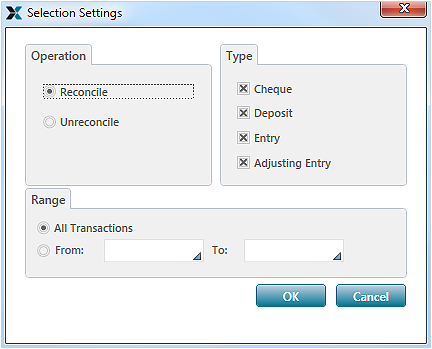

. The Selection Settings window is displayed.

. The Selection Settings window is displayed.

- In the Operation group, select Reconcile.

- Select the options that correspond to the types of transaction to reconcile: cheque, deposit, entry and adjusting entry.

- Define the range of transactions to include in the reconciliation: All transactions or the transactions included in a range of dates.

- Click OK. In the Reconciliation window, the parameters are applied at the same time on the transactions.

- Back to the Reconciliation window, click

. The reconciliation is added to the list of reconciliations. The Reconciliation window remains displayed in order to make modifications if required.

. The reconciliation is added to the list of reconciliations. The Reconciliation window remains displayed in order to make modifications if required.

Aide mémoire

Hide

the reconciled transactions.

Display

all previously hidden reconciled transactions.

Display

postdated transactions.

Produce

the reconciliation report. This report can be used to view the list of outstanding transactions after the reconciliation, to make sure that the balances in the books match those of the bank statement and that no transaction associated with the account was forgotten.